If you don’t yet receive Tanay's newsletter in your email inbox, join the 10,000+ subscribers who do: Subscribe now

ServiceTitan just filed for its IPO a few weeks ago, and there's a lot to unpack here. For those unfamiliar, ServiceTitan is a leading SaaS provider for the trades—think HVAC technicians, plumbers, electricians. This filing represents a major step for the company, and it's a good opportunity to understand its journey, financials, and vision for the future as well as some of the interesting dynamics around structure on later-stage rounds and the impact of it.

I'll discuss:

- Overview

- Product Suite

- Financials Metrics and Growth

- Margins and Profitability

- IPO Valuation and Timing

- Closing Thoughts

Let's get into it.

I. Overview of the Business & Market Opportunity for ServiceTitan

ServiceTitan operates within the vast trades industry—serving the plumbers, electricians, HVAC technicians, and other critical tradespeople that ensure people’s daily lives function smoothly. ServiceTitan aims to be the premier operating system for these trade service providers, offering end-to-end solutions that integrate key workflows under one platform. By addressing core pain points in customer relationship management (CRM) , field service management (FSM), and enterprise resource planning (ERP), ServiceTitan has established itself as a crucial tool for driving operational efficiency and profitability within this historically under-served market.

ServiceTitan represents the classic “Vertical SaaS playbook” executed well. The company is at ~$772M implied ARR and estimates their current serviceable market opportunity at $13 billion, assuming a capture rate of 2% of the GTV in the trades.

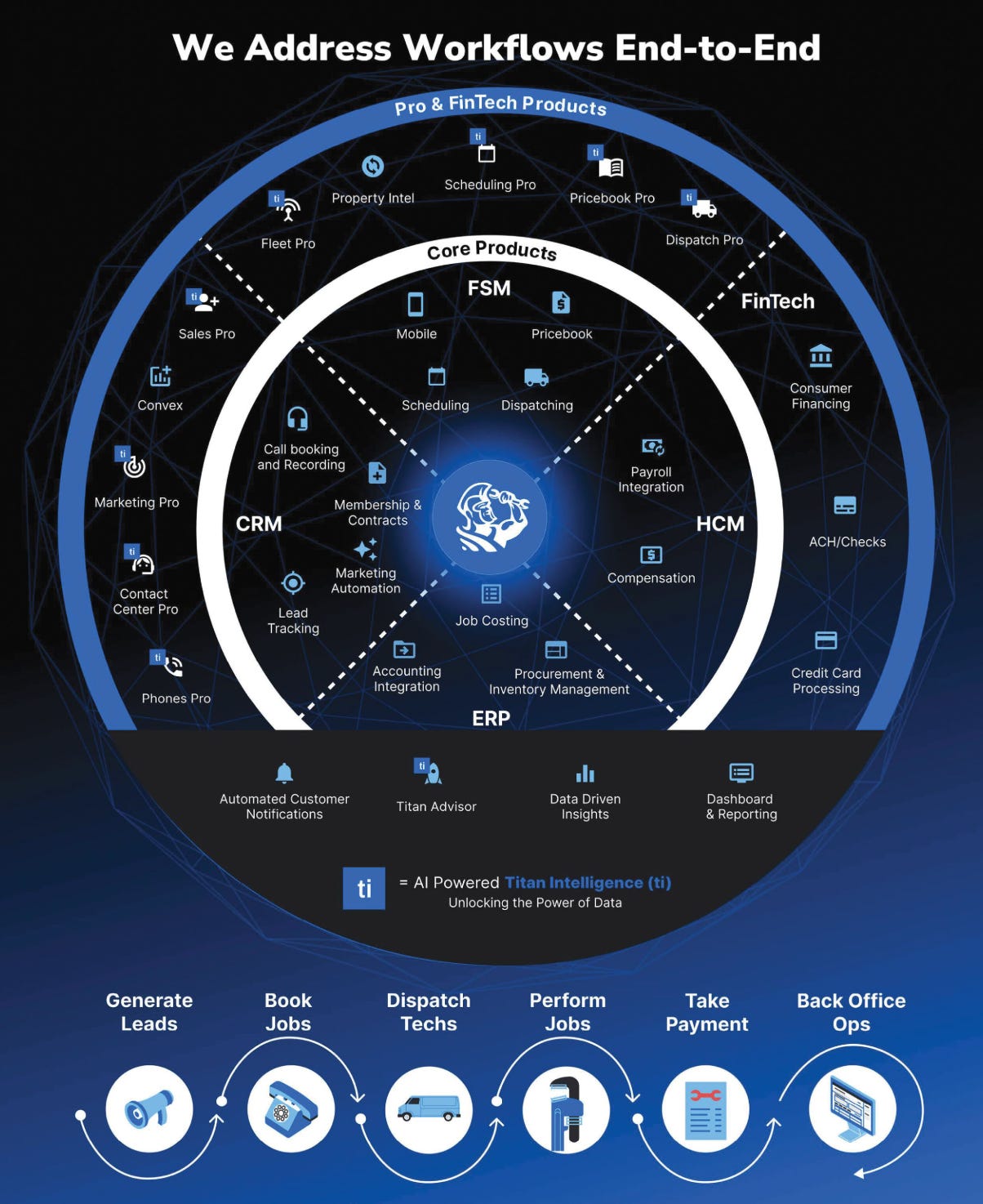

II. ServiceTitan's Product Suite

ServiceTitan has positioned itself as the premier software provider for the trades industry by offering a comprehensive suite of cloud-based solutions for managing key workflows. Their product strategy follows a classic vertical SaaS playbook, offering a core product that covers foundational business needs and add-on solutions, including fintech ones, that deepen customer engagement over time.

Their goal is to help owners of these businesses in the trades i) accelerate growth, ii) drive operational efficiencies and iii) deliver a superior end-customer and field service technician experience in their business.

ServiceTitan’s platform includes a suite of products and features aimed at helping trade businesses with a few key goals:

- Accelerate Revenue. Tools to help inform customer targeting and market those end customers.

- Drive Operational Efficiency. Tools to reduce operational burdens in booking and payments.

- Deliver a Superior End-Customer Service Experience. Tools to deliver better and modern experiences to end customers from the initial call to scheduling to reviews.

The product can be broken down into 3 components:

- Core product, which offers a base-level functionality across all key workflows, including call tracking, scheduling, dispatching, end-customer communications, marketing automation, estimating, job costing, sales, inventory and payroll integration.

- Pro Products which provide advanced functionality in areas such as marketing, pricing, dispatch and scheduling

- FinTech products which include third-party payment processing and third-party financing solutions, which enable ServiceTitan to monetise the payment volume through their platform.

This tiered approach allows ServiceTitan to attract customers with a comprehensive Core offering and drive further revenue growth through the adoption of higher-value add-on products.

III. ServiceTitan Financial Metrics & Growth

ServiceTitan has been growing steadily and is at some real scale. For the 12 months ending July 31, 2024, ServiceTitan reported $685M in revenue, reflecting year-over-year growth of 24%, and an implied ARR of $772M. They grew at a CAGR of 50%, from $179.2M to $614.3M from end of 2020 to end of 2023.

ServiceTitan makes revenue in 3 ways:

- subscription revenue on their core and pro products

- usage based revenue on transaction volume through payment processing

- professional services revenue

The split of revenue has been relatively stable over time, as below. Subscription revenue is ~70%, Usage revenue is ~25% and professional services is the rest.

Its clear that the fintech component is important, with usage based revenue at 25% of overall revenue. The gross transaction volume through ServiceTitan’s platform is now $62B in the last twelve months and is growing at slightly below overall revenue growth. This represents the total invoiced by their customers to end-users. At the same time, the take rate on that revenue that ServiceTitan has been able to generate from payment processing, etc has roughly been constant at 0.25% over time. On an aggregate basis, ServiceTitan’s revenue is roughly 1% of the GTV it enables.

On the retention front, ServiceTitan is pretty strong given how core the offering is as the “OS” for the businesses that use it.

- Gross retention has been >95% over the last 10 quarters, indicating how sticky it the product is.

- Net dollar retention has been >110% over the last 10 quarters, which is strong for a SMB vertical SaaS, but indicates a limit to size and scope of expansion in these accounts, and they note a 7 percentage point decrease in that period with scale. This expansion tends to be driven by increased usage based revenue as well as upgrading to pro products.

IV. Margins and Efficiency

ServiceTitan’s path to profitability is still under construction (at least on a GAAP basis), but they have been making significant improvements on their margins.

Their Gross Margins have gone up from the ~55% to 65% percent (with their gross margin on just their platform up to 74%), and they have reduced all three of R&D, G&A and Sales and Marketing as a percent of revenue over time.

In particular, they call out a focus on growing their gross margins and also reducing G&A as a percent of revenue through focus on efficiency of their processes and systems over time.

From a non-GAAP perspective, they did make an income from operations in the six months ending July 2024, of $16.8M, with a non-GAAP operating margin of 5%. If we use that as a proxy to calculate the Rule of 40, that puts ServiceTitan at 29% on the Rule of 40.

V. IPO Valuation and IPO Timing

ServiceTitan has indicated that they intend to sell 8.8M shares as part of the IPO, at an offering price in the region of $54.50 per share, which would allow them to raise ~$480M of capital. Depending on where it lands, this will put them in the ~$6B or so market cap range, and have them trading at 7-7.5x NTM revenue.

Prior to this IPO, they had raised $1.4B in equity capital, with some of the key shareholders in the company including ICONIQ Growth (24% of Class-A shares), Bessemer (13.9%) and Battery (7.5%).

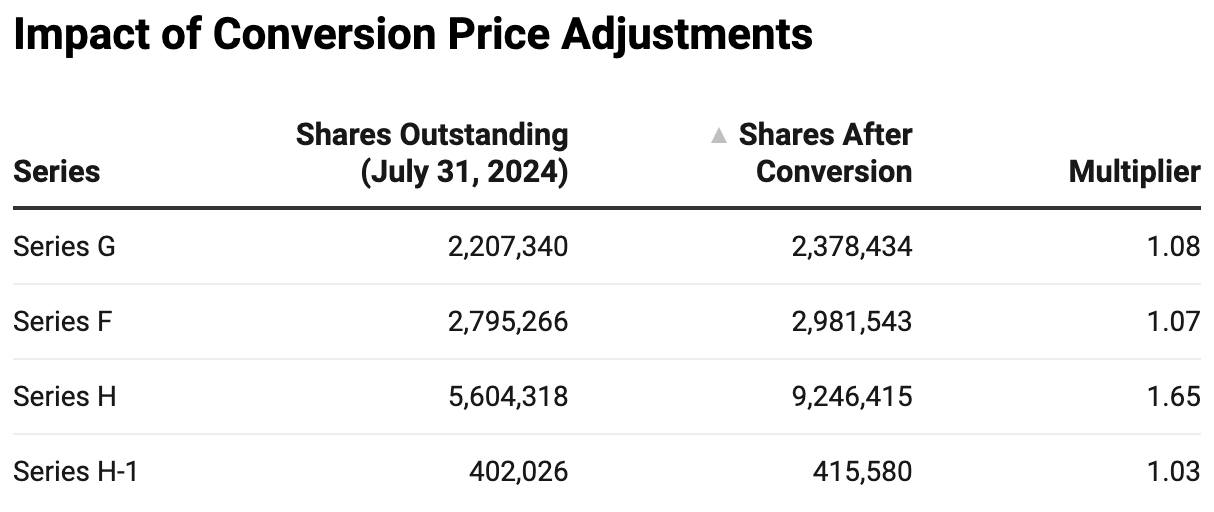

Interestingly, as part of later rounds, there was some structure put in the rounds, which protected investors from an IPO below certain valuation threshholds.

One aspect of it was a conversion price adjustment to the number of shares issued for IPOs under $85/share, which is what we have happening here.

The Series F, Series G and Series H-1 redeemable convertible preferred stock are entitled to a conversion price adjustment in the event the initial public offering price is less than $105.0878 per share, $115.7635 per share and $84.5712 per share, respectively, based on a broad-based weighted average calculation

In addition, as part of the Series-H, there was a similar clause, which had the price adjustment factor compounding at 11% per year, starting May of this year, in what was essentially a “compounding ratchet”.

The Series H redeemable convertible preferred stock is entitled to a conversion price adjustment in the event the initial public offering price is less than $84.5712 per share, accreting at a rate of 11% per annum, accruing daily and compounding quarterly from and after May 22, 2024, or the Ratchet Adjustment Denominator. The updated conversion price for the Series H redeemable convertible preferred stock is determined by multiplying (i) the initial public offering price by (ii) $84.5712 divided by the Ratchet Adjustment Denominator.

This may have been one of the reasons for ServiceTitan to go public sooner rather than later, since the longer they waited, the more dilutive this Series H round would end up being for them.

Since ServiceTitan is going public under $85 per share, investors in the Series F,G and H all get additional shares, as illustrated below. One simple way to understand the implications of this, is that instead of being issued ~11M shares, these investors will get issued ~15M shares, representing an addition ~4% dilution to the company.

Had ServiceTitan waited say another year or two to go public, its possible that the Series H holders would get another ~1-1.5M or so shares, implying another 1%+ dilution.

In addition, ServiceTitan had raised $250M in the form of non-convertible preferred stock in October 2022 from Saturn FD and Coatue Tactical Solutions, which it intends to use ~$310M from the IPO proceeds to purchase at cost plus accrued dividends, which otherwise would continue to accrue dividends at 10% per year for the first five years and 15% the year after.

VI. Closing Thoughts

ServiceTitan had humble beginnings selling software products to the plumbing trade for residential homes and has since expanded its product offering into a full-fledged platform, and serves all the trades including HVAC, electrical, landscaping and others. It is an extremely important product to its customer that is growing steadily in a market that has been historically been under penetrated and digitized, and there’s certainly room for it to continue to grow, although the markets will likely continue to question it on how much of their stated $13B TAM remains addressable and on their profitability trajectory given growth rates.

Congrats to the ServiceTitan team as they gear up for the IPO, and it will be interesting to watch how it trades and continues to perform in the public markets!

If you're interested in this sort of content in your inbox, check out my Substack.